This week, the magnesium industry chain as a whole showed a sideways consolidation pattern, with price fluctuations of various products narrowing.

Dolomite: Recently, downstream magnesium plants have gradually resumed production, especially the resumption of high-quality magnesium ingot production in Shaanxi, which has driven up the demand for high-quality dolomite. However, due to ample capacity in regions such as Wenxi in Shanxi, Hubei, and Inner Mongolia, coupled with sufficient inventory reserves despite shutdowns in Wutai, the supply of high-quality dolomite remains abundant. It is expected that prices will remain stable going forward. In the ferrosilicon market, futures prices fluctuated significantly this period, with the most-traded 2509 contract reaching a weekly high of 5,455 yuan (up 178 yuan MoM) and a low of 5,204 yuan (down 120 yuan MoM). The spot market, affected by weak off-season demand, saw a slowdown in supply and demand, with sluggish trading activity. Prices are expected to maintain a steady trend in the short term.

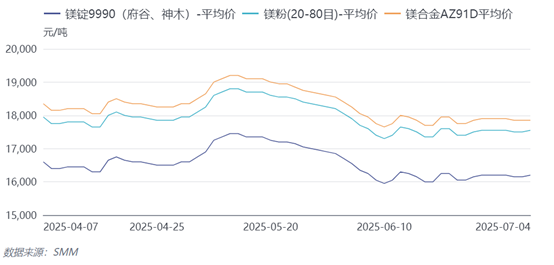

Magnesium ingot: As of the time of writing, the transaction price of 99.90% magnesium ingot in the main producing area was 16,200 yuan/mt, with FOB quotes at $2,260/mt. This week, the magnesium ingot market continued to fluctuate rangebound, with prices consistently oscillating within the 16,000-16,300 yuan/mt range, showing a clear sideways consolidation. Supply remained stable, but the expectation of production resumptions in July brings potential pressure. On the domestic trade side, just-in-time procurement provided limited support, while foreign trade remained depressed due to the European summer break and economic downturn, leading traders to purchase as needed. Although some magnesium producers attempted to refuse to budge on prices at the beginning of the week, strong desire to bargain down prices from downstream buyers and rising inventory pressure led to a slight downward shift in actual transaction centers. The overall market maintained a dual-weakness in supply and demand, with factories' reluctance to budge on prices and traders' cautious purchasing continuing to be at odds. It is expected that the market will continue to show a weak consolidation trend in the short term.

Magnesium alloy: As of the time of writing, magnesium alloy prices were quoted at 17,800-17,900 yuan/mt, with FOB quotes at $2,505/mt. Recently, major magnesium alloy producers have continuously expanded their capacity, increasing supply, and competition in processing fees has intensified, with current levels already hovering at a low. With the onset of the die-casting industry's off-season, magnesium alloy orders have decreased, and weak demand-side support has increased inventory pressure for manufacturers. Coupled with the narrow fluctuation in raw material magnesium ingot prices, the market trading atmosphere is rather sluggish. It is expected that magnesium alloy processing fees will continue to operate in the doldrums, with prices showing a narrow fluctuation pattern.

Magnesium powder: As of the time of writing, magnesium powder prices were quoted at 17,550 yuan/mt, with FOB quotes at $2,415/mt. Magnesium powder prices remained stable overall, with raw material cost support still present. The domestic market mainly focused on just-in-time procurement, with downstream enterprises being cautious about restocking; the overseas market entered the traditional summer break, with a noticeable decline in inquiry activity and a sluggish trading atmosphere. Producers generally produced according to orders, maintaining only a small amount of working inventory, with a strong wait-and-see sentiment in the market. Although the decline in raw material prices has brought certain pressure, buyers and sellers continue to engage in a game of negotiation, maintaining an overall weak but stable operation trend.